The Wine Industry Is Misdiagnosing the DtC Slowdown: Why Omnichannel Retail Changes Everything

Over the past several years, I have watched an increasing amount of discussion in the American wine industry focus on one central question:

“How do we improve the winery DtC experience?”

The industry has invested heavily in improving hospitality, CRM, digital marketing, wine clubs, and experiential programming. Those investments matter. In fact, wineries that have not implemented structured systems for improving the DtC customer journey are already falling behind.

Yet despite these efforts, DtC sales continue to underperform broader market trends particularly in key premium price segments.

According to Wine Business Analytics, DtC shipment value declined nearly 5% in the most recent twelve-month period ending April 2026 while volume fell more than 15%, representing a loss of roughly one million cases. More concerning, declines were concentrated in the very price segments that historically fueled DtC growth, while gains increasingly came from bottles above $100.

This is why I believe much of the industry is misdiagnosing the underlying DtC issue.

The wine industry still discusses DtC as though wineries are competing primarily against other wineries for the digital dollar. I increasingly believe that assumption is outdated.

The core challenge facing winery DtC today is not simply that wineries need to create different experiences. It is that the original structural advantages of winery DtC have fundamentally changed.

In 2005, following the landmark Supreme Court decision in Granholm v. Heald, American winery DtC possessed two enormous advantages:

Scarcity and access

Convenience

Consumers joined wine clubs and purchased directly from wineries because many wines simply were not available locally. Even when they were available, the winery often provided the easiest and most reliable access point, and having these wines delivered directly to your door (even if it meant waiting months because of a “heat hold”) was novel and exciting.

Today, consumers increasingly live inside omnichannel digital retail systems with broad product access and quick delivery.

A consumer in Southern California can decide right now to host a dinner party this evening, open the Albertsons or Pavilions app, order groceries, flowers, desserts, and high-quality premium wine in a single transaction, and have everything delivered today before guests arrive.

In Texas, H-E-B has built a deeply integrated ecosystem around curbside pickup, grocery delivery, and rapid beer and wine fulfillment through Favor.

According to a recent article by Vinetur, digital sales now represent approximately 18% of Total Wine & More's revenue, while 65% of customers begin their purchasing journey online. The company’s website receives more than 190 million visits each year. Its mobile app has been downloaded about 7 million times and has around 1.8 million monthly users.

Instacart and similar delivery platforms allow consumers to seamlessly add a selection from Total Wine or their favorite neighborhood retailer into the same broader purchase order as grocery and non-food items, receiving them all at once.

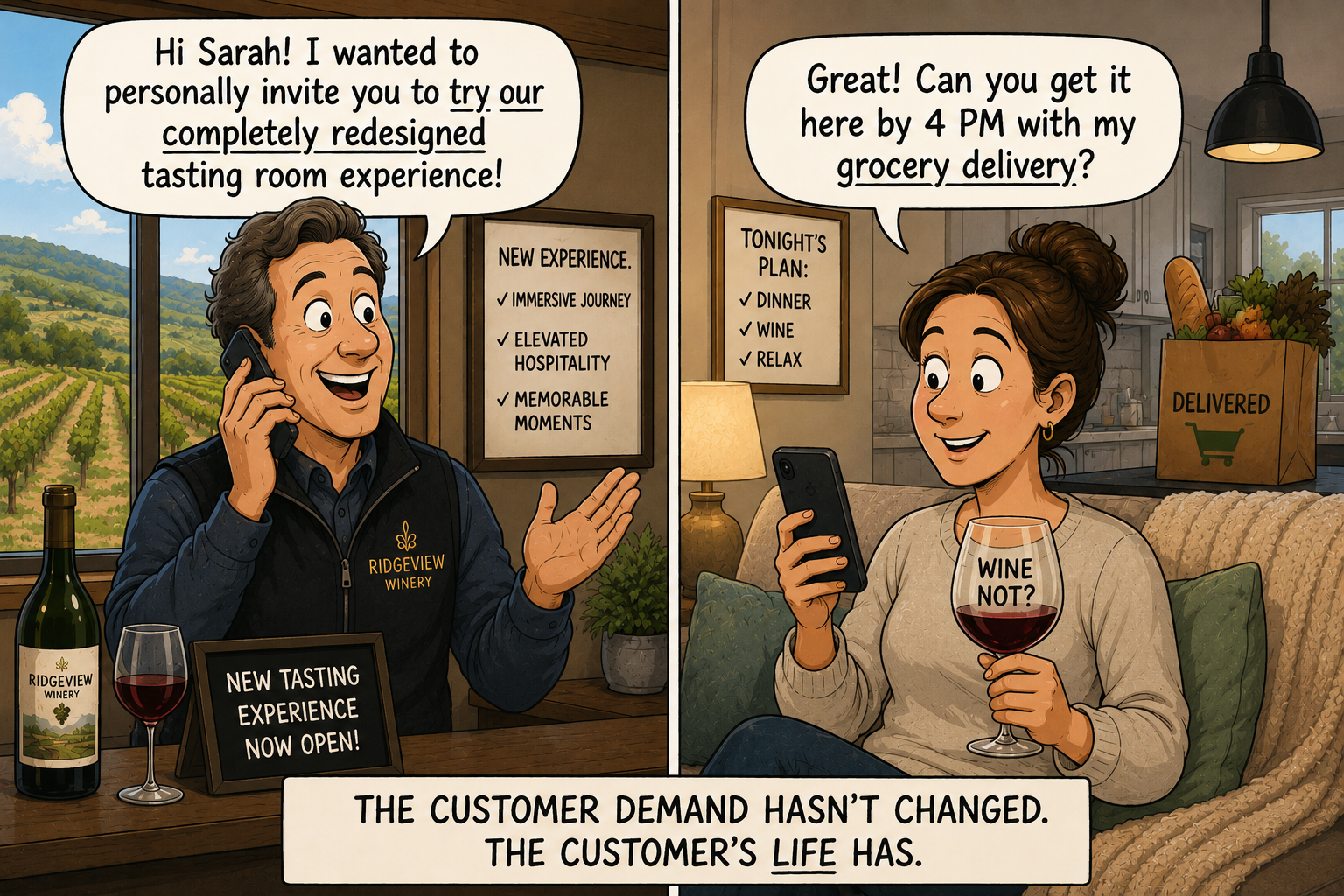

The premium DtC customer who was formerly driving $20-$50 online direct-from-winery purchases has not necessarily changed her demand behavior. Her life has changed.

Meeting the customer where they are is both physical and mental, and omnichannel retail feeds that need.

Importantly, this behavior is no longer limited to large national chains.

Binny's Beverage Depot in Illinois allows consumers to browse more than 25,000 products, check local inventory, receive recommendations, place pickup orders, and arrange same-day delivery from a mobile device.

Similar capabilities are increasingly available nationally through independent neighborhood retailers, who not only offer the same digital and logistical advantages, but have access to highly curated, artisan wines and develop direct customer relationships with their neighbors.

In terms of both logistics and access, the advantages created by Granholm v. Heald are simply no longer the same as they were in 2005.

At the same time, product access and discovery through wholesale channels have expanded dramatically, even as the overall wine market has contracted in recent years. Imported wines represented roughly one-quarter of U.S. wine consumption twenty years ago. Today they account for closer to 35–40% of the market, with dramatically improved quality, availability, and digital accessibility.

Consumers no longer need to join individual winery clubs or subscription services simply to access discovery. Today they can browse English sparkling wine, Rioja, amazing values from Portugal, premium Cava, boutique domestic producers, and thousands of other wines from a mobile device, often with same-day delivery.

For years, many wineries viewed their competitive set as neighboring tasting rooms, similar wine clubs, or regional peer luxury brands. That is no longer the complete picture.

Ironically, that is not necessarily bad news for American wineries.

Unlike many feared during the rise of ecommerce, these retailers are not replacing winery DtC relationships. Increasingly, they are becoming part of the broader wholesale-DtC ecosystem.

One thing that hasn't changed is that today's premium wine customer journey often starts with a consumer discovering a winery through retail or a restaurant, especially by-the-glass. That discovery may lead to a winery visit or simply an Instagram handle lookup, hopefully a wine club membership and future retail purchases, and eventually purchases across multiple channels simultaneously.

The future of wine sales is not DtC or wholesale.

It is both.

The industry often frames wholesale as something wineries reluctantly pursue only after maximizing DtC profitability. I believe that framing misunderstands both scalability and consumer behavior. It certainly misunderstands the data, which clearly shows that wholesale accounts for the vast majority of wine sales in the U.S.

I have written previously about the difference between gross margin and contribution margin. The reality is that despite DtC gross margins, most scalable wine brands eventually become wholesale-dominant businesses by volume, and Silicon Valley Bank's research suggests that transition begins surprisingly early in a successful winery's growth trajectory (after about 2,500 cases).

The strongest wine businesses increasingly think in ecosystems:

• DtC builds loyalty and data. • Wholesale builds visibility and convenience. • Retail builds frequency. • Restaurant, bar and hotel features build cultural relevance. • Digital commerce connects them all together.

Ironically, the rise of omnichannel retail may actually reinforce the long-term importance of the three-tier system rather than weaken it. Consumers still want convenience, discovery, local availability, and frictionless purchasing. They simply expect all of it to happen faster and more seamlessly than ever before.

Wineries should absolutely continue improving hospitality and the DtC experience. In fact, the rise of sophisticated omnichannel retail means there is now even less room for error when it comes to winery hospitality, CRM, and digital marketing. When a customer can open their favorite grocery store app and quickly access high quality products, wineries cannot afford to let visitors pass through their doors without creating a memorable experience and emotional connection, and they can't afford a lack of systems and processes for converting future sales when that customer goes back home.

But hospitality innovation alone is not the solution to declining DtC share in critical price segments.

The industry must stop treating DtC and wholesale as opposing strategies and instead build systems where success in one channel strengthens success in the other. The future belongs to wineries that understand and maximize the wholesale-DtC ecosystem.

Don’t know where to start or need to strengthen your wholesale muscle? M. Learning Academy is the place.

An ecosystem of online purchasing is the world where today’s premium wine consumer lives. Meet her there and you will succeed.